Energy Transformation: The Future of Green Energy Vehicle

Industrial energy transition has become the top priority for sustainable development as well as key parameters across industries. Increasing the proportion of renewable and non-fossil energy, while enhancing technological safety, efficiency, and widespread adoption, can reduce carbon dioxide emissions and promote climate change governance.

China is undergoing major energy transformation. It aims that by 2024, energy consumption per unit of GDP will be reduced by approximately 2.5%. Energy-saving and carbon-reduction transformations in key fields and industries will result in energy savings equivalent to about 50 million tons of standard coal and reduce carbon dioxide emissions by about 130 million tons (The State Council, 2024).

Looking forward, the proportion of non-fossil energy consumption will reach 20% from XX%. The industrial energy development goals mentioned above, while promoting industrial economic development, are ushering in a new era of energy by the end of 2025 (The State Council, 2024).

New Era of Zero Carbon Park

Industrial energy transition has become the top priority for sustainable development as well as key parameters across industries. Increasing the proportion of renewable and non-fossil energy, while enhancing technological safety, efficiency, and widespread adoption, can reduce carbon dioxide emissions and promote climate change governance.

China is undergoing major energy transformation. It aims that by 2024, energy consumption per unit of GDP will be reduced by approximately 2.5%. Energy-saving and carbon-reduction transformations in key fields and industries will result in energy savings equivalent to about 50 million tons of standard coal and reduce carbon dioxide emissions by about 130 million tons (The State Council, 2024).

Looking forward, the proportion of non-fossil energy consumption will reach 20% from XX%. The industrial energy development goals mentioned above, while promoting industrial economic development, are ushering in a new era of energy by the end of 2025 (The State Council, 2024).

New Era of Zero Carbon Park

Zero Carbon Park represents the major progress of energy transition from traditional fossil fuel into electricity. Starting on December 12, 2024, the Central Economic Work Conference for the first time proposed 'Zero Carbon Parks.' This refers to modernized industrial parks that, within a specific cycle (typically one year), offset all carbon emissions through clean technology support, carbon recovery technology, energy storage and exchange, and other means, thereby achieving 'net zero emissions' of carbon elements for the entire year.

Figure1. Taken by Xinhua News Agency at Ordos, one of the twelve subdivisions of

Inner Mongolia, China.

The most classic example of a zero-carbon park is the Ordos Zero Carbon Industrial Park, created in 2022 by the Ordos government and Envision Group as the world's first zero-carbon park. This park features a 100% zero carbon energy system, with 80% of its energy coming from on-site wind power, photovoltaics, and storage, while the remaining 20% is supplemented through green electricity trading (Zhang, 2024).

According to the plan, by 2025, with a low-carbon consumption of 10 billion kWh, the Ordos Zero-Carbon Industrial Park will account for approximately 12% of the total new energy consumption in Ordos (China Association of Automobile Manufacturers, n.d., 2025).

Policy Development and Iteration in China's New Energy Industry in Recent Years

Along with technological transformation, supportive policies are also implemented to promote market growth. From 2017 to 2020, subsidy standards for all vehicle models, except for fuel cell vehicles, showed a clear downward trend. Specifically: in 2017-2018, the subsidy standard was reduced by 20% compared to the 2016 baseline, and in 2019-2020, it was reduced by 40% from the 2016 baseline. (National Development and Reform Commission et al., 2024)

International Market Penetration

Amidst rapid market development in recent years, and through the vigorous promotion of the international influence of China's new energy technology and a broad increase in global market penetration, the export share of new Chinese energy vehicles reached 44.5% as of May 2025 (Baijiahao, n.d.). Compared to the 20.6% export share in 2020, this demonstrates a more than double increase and demonstrates the significant influence and potential of China's new energy vehicles in the international market.

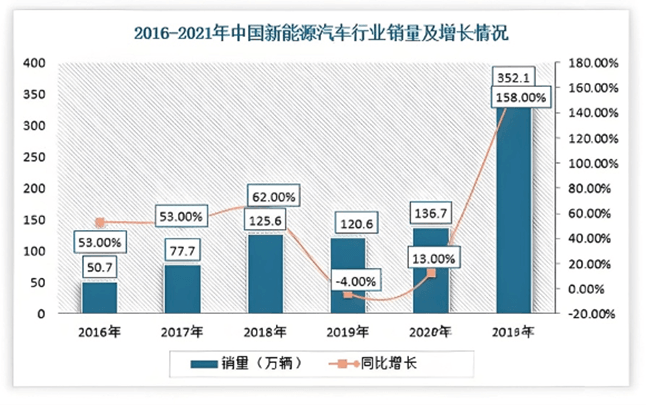

Figure 2. The year-on-year growth rate (%) plotted on a time scale from 2016 to 2020 After hitting rock bottom in sales in 2019, the Chinese new energy vehicle market began to soar exponentially in 2020.

Maximizing the utility of each life-stage for Lithium-Ion Battery

Today, new energy vehicles are accounting for an increasingly larger share of the market. At the same time, vehicle owners and manufacturers are beginning to face the next-stage challenge of electric vehicle processing and recycling. How can we ensure that these vehicles not only serve their purpose during their operational lifespan but also continue to deliver maximum benefits after they have completed their service life?

By the end of 2024, the number of NEVs in use in China had reached a staggering 31.4 million, accounting for 8.9% of the country's total vehicle fleet. In contrast, the United States had only 4.5 million NEVs during the same period, representing less than 2% of its total vehicles. Germany and Japan, ranking as the world's third and fourth largest NEV markets, had only 2.8 million and 2.3 million units, respectively (Xinhua News Agency, 2025). Given such a massive market, safe, efficient, and comprehensive end-of-life vehicle processing procedures and workflows have become critically important. Power batteries, which contain numerous pollutants such as lithium, represent the most significant challenge in NEV recycling. Maximizing the environmentally friendly utilization of these batteries and other hazardous components becomes the main issue to be tackled for the industry.

Mainstream Recycling Methods of Lithium Battery

1. Second-Life Utilization

Second-life utilization refers to the process by which retired power batteries undergo systematic procedures—such as disassembly, categorization, electrochemical performance evaluation, module reconfiguration, and reassembly—to be redeployed in application scenarios with comparatively lower performance requirements. Typical end uses include telecommunications base-station backup power, stationary energy storage systems, and low-speed electric mobility.

One prime example of battery that is suitable for second-life utilization is Lithium iron phosphate (LFP) batteries, characterized by relatively low concentrations of high-value metals, offer limited economic incentives for direct material recovery. However, their high thermal stability and elevated self-ignition temperature afford strong intrinsic safety even after noticeable capacity fade, rendering them particularly suitable for second-life deployment.

2. Regenerative Recycling (Material Recovery)

Regenerative recycling involves the comprehensive treatment of end-of-life power batteries through processes such as mechanical disassembly, crushing, physical separation, material refurbishment, and subsequent metallurgical extraction (e.g., hydrometallurgical or pyrometallurgical methods). This pathway enables the recovery of high-value metal constituents—including lithium, cobalt, and nickel—and supports the closed-loop reutilization of critical battery materials.

Vehicle-Level Recycling Process

Automation Recycling State

Stage 1

Following the removal of the traction battery in the battery disassembly system, the vehicle is transferred to the pre-treatment unit, where hazardous components and reusable parts are systematically dismantled and recovered.

Stage 2

After hazardous materials and recoverable components have been removed, the vehicle is connected to the fluid-draining system for the extraction of all residual liquids. Subsequently, operational and non-operational vehicles are routed to distinct processing streams.

Stage 3

Operational vehicles are transported via forklift to the supervised destruction system, whereas non-operational vehicles are directed immediately to the shredding system. Upon completion of supervised destruction, operational vehicles are likewise delivered to the shredding system.

Stage 4

Materials produced from the shredding process—regardless of vehicle operational status—are conveyed to the sorting system for downstream treatment.

Stage 5

The sorting system separates the shredded output into waste steel, stainless steel, wire ends, printed circuit boards, plastics, rubber, and non-ferrous metals. These material fractions are then forwarded to specialized facilities for further recovery and resource reutilization.

Manual Disassembly Stage

Stage 1

Recovery of Reusable Components: Components with remanufacturing or secondary-use potential—such as headlights, electric motors, and other serviceable parts—are dismantled and recovered for vehicle repair or redistribution in the second-hand market.

Stage 2

Handling of Hazardous Components: Hazardous parts, including catalytic converters and lead–acid starter batteries, are removed and transferred to certified facilities for compliant hazardous-waste treatment (Wang, et al,.2024).

Key advantages in the recycling of power batteries and end-of-life vehicles

1. High-efficiency shredding and sorting technologies ensure the quality and purity of recovered materials, achieving an overall material recovery rate exceeding 97%.

2. Advanced shredding equipment enables continuous operation, reducing energy consumption and significantly extending equipment lifespan, thereby enhancing process stability and economic efficiency.

3. Finally, a high level of automation substantially reduces labor requirements, decreasing operator workload while improving processing efficiency and safety (Wang, et al,.2024).

Recycling Approaches for Vehicle Components

One of the key advantages of electric vehicles is its recyclability. Almost every major part—tires, metal frames, interior components—can be recycled with specialized procedures. The advancement in recycling technologies improves the efficiency and cost-benefit of recycling components, maximizing their utility while minimizing environmental damage. The recycle is categorized into three major components:

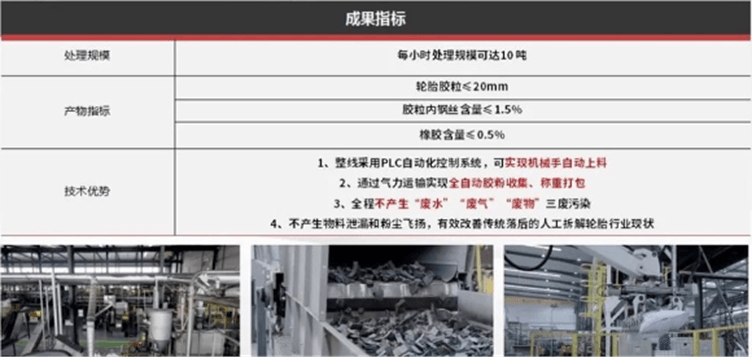

1. Tires: Modern automated processing lines can handle entire tires—including truck, large, and passenger tires—through an integrated treatment workflow. The system separates steel wires, fibers, and rubber granules. The rubber granules can be further valorized through pyrolysis to produce oil and carbon black or processed into fine rubber powder for industrial applications (Wen Liang, 2023).

Figure 3. The treatment scale over 10 tons per hour and several technical

advantages including PLC automation, elimination of wastewater, gas, and

materials, and fully automated collection and weighing.

2. Vehicle Body Metals: Vehicle bodies and non-manufacturable components are first shredded and then sequentially processed through magnetic separation (ferrous metals), trommel screening (particle size classification), air separation (light materials), eddy current separation (non-ferrous metals), and induction sorting (stainless steel), enabling efficient recovery of all metal fractions.

3. Seats and Interior Materials (Non-Metallic): Lightweight non-metallic materials such as plastics, foams, and fabrics are separated via air classification. Recovered plastics may be recycled into low-end plastic products, while high-calorific-value materials can be utilized for energy recovery (Xu & Zhou, 2019).

Divergence of Development between China and International Industry

Charging Infrastructure

China has made significant breakthroughs in ultra-fast charging technology, achieving core parameters of 1000 kW charging power, 1000 V voltage, and 1000 A current (BYD, 2025). For instance, BYD’s technology enables a 400 km driving range after only five minutes of charging (BYD, 2025). Charging infrastructure is also being built at an extraordinary pace. By 2025, the number of charging stations in China is projected to exceed 8 million (State Council of the People’s Republic of China, 2025).

In contrast, the United States suffers from insufficient charging coverage, particularly in central desert regions. These gaps can be especially visible in geographically isolated regions, including desert areas such as Imperial County in Southeastern California, which has been identified as lacking adequate charging availability relative to need (CalMatters, 2024). On the battery supply side, U.S. domestic industry captures less than 30% of the economic value of battery cells consumed in the U.S. market, indicating continued dependence on imported materials and components (Li-Bridge, 2023). Meanwhile, Chinese battery supply dominates globally: China controls over 75% of global cell production capacity, reflecting its outsized role in the world power-battery supply chain (Li-Bridge, 2023).

Intelligent Driving

China leverages full-industry-chain advantages and policy support to accelerate the deployment of advanced driver-assistance systems (ADAS) and the mass production of Level 3 (L3) autonomous vehicles (MIIT, 2023; McKinsey & Company, 2024). Major technology firms such as Huawei and Baidu have implemented vehicle–road–cloud integrated autonomous driving solutions, combining onboard intelligence, roadside infrastructure, and cloud-based data processing (Baidu, 2023). Companies such as Huawei and Baidu have implemented “vehicle–road–cloud integrated” solutions, conducting autonomous driving tests in complex urban environments in cities including Guangzhou and Shanghai.

U.S. companies focus on optimizing single-vehicle intelligence. Tesla’s Full Self-Driving (FSD) V13 utilizes a pure vision-based approach to achieve “hands-free” driving, with neural networks directly processing camera inputs, minimizing reliance on high-precision maps and LiDAR (Tesla, 2024). Waymo employs extensive simulation testing, accumulating over 20 billion virtual miles to enhance algorithmic robustness in extreme scenarios (Waymo. 2023).

Industrial andEnvironmental Policies

Figure4. “Apollo Go” Autonomous Vehicle Operations.

The system has been deployed and is currently operational in several cities,

including Beijing, Wuhan, and Shenzhen.

The government is actively supporting the development of intelligent, connected highway infrastructure nationwide, facilitating large-scale deployment of vehicle–road collaborative systems. For example, to promote the commercialization of Level 3 (L3) autonomous driving, cities such as Beijing and Wuhan have enacted the Autonomous Vehicle Regulations (Apollo, n.d.).

On the other hand, the United States lacks a unified federal framework for autonomous vehicles, resulting in significant policy variation across states. For example, California permits autonomous vehicle testing, whereas Texas and Florida maintain strict prohibitions (UrbanSDK, 2025; AVFRST, 2025).

As the world’s largest industrial nation, China assumes a leading role in promoting green economic transformation and reducing overall energy consumption through comprehensive carbon-reduction strategies, systematic policy frameworks, and accelerated renewable energy development that contribute to global climate action (State Council of the People’s Republic of China, 2025). Its policy initiatives not only serve as a model for most countries but also align with the global governance concept of a “community with a shared future for mankind”, reflecting broad international consensus on climate responsibility.

Reference

Apollo. (n.d.). Intelligent driving system – Baidu Apollo autonomous driving open platform [Apollo.auto] https://www.apollo.auto/apollo-self-driving

AVFRST. (2025). Automated driving regulations – where are we now? https://www.avfrst.com/Regulatory/

Baidu. (2023). Apollo autonomous driving open platform: Vehicle–road–cloud integration in urban mobility. https://apollo.auto

Baijiahao. (n.d.). From January to May 2025, China's auto sales reached 12.748 million units, with new energy vehicles accounting for 44% [2025年1-5月我国汽车销量达1274.8万辆,新能源车占比44%]. Baidu. Retrieved November 12, 2025, from https://baijiahao.baidu.com/s?id=1834612934141871571&wfr=spider&for=pc

BYD. (2025, March 18). BYD unveils Super e-Platform with megawatt flash charging for electric vehicles, matching refueling speeds.

China Association of Automobile Manufacturers. (n.d.). 2016 – 2020 新能源车补贴政策分析 [Analysis of new energy vehicle subsidy policies from 2016 to 2020]. http://www.caam.org.cn/chn/9/cate_107/con_5156926.html

Harvard Business School. (2024, June 26). The state of EV charging in America.

Li-Bridge. (2023, March). Building a robust and resilient U.S. lithium battery supply chain (Report). U.S. Department of Energy, National Energy Technology Laboratory.

McKinsey & Company. (2024). Autonomous driving in China: Scaling ADAS and L3 deployment. https://www.mckinsey.com

Ministry of Industry and Information Technology of the People’s Republic of China (MIIT). (2023). Guidelines for the development of intelligent connected vehicles. https://www.miit.gov.cn

Mission of China to the United Nations. (2025, November 5). Striving for the building of a community with a shared future for humanity. https://un.china-mission.gov.cn/eng/zgyw/202511/t20251126_11760388.htm

National Development and Reform Commission. (2024, August 8). 关于进一步强化碳达峰碳中和标准计量体系建设行动方案(2024—2025年)的通知(发改环资〔2024〕1046号) [Guānyú jìnyībù qiánghuà tàn dáfēng tàn zhōng hé biāozhǔn jìliàng tǐxì jiànshè xíngdòng fāng'àn (2024—2025 nián) de tōngzhī (fā gǎi huán zī〔2024〕1046 hào), Notice on the action plan for further strengthening the construction of standard and measurement systems for carbon peaking and carbon neutrality (2024-2025) (NDRC Env. Res. [2024] No. 1046)]. https://www.ndrc.gov.cn/xxgk/zcfb/tz/202408/t20240808_1392291.html

State Council of the People’s Republic of China. (2025, December 23). China's EV charging infrastructure reports robust growth.

Tesla. (2024). Full Self-Driving (FSD) beta V13 release notes. https://www.tesla.com

The State Council. (2024, May 29). 《2024—2025年节能降碳行动方案》 [Energy Saving and Carbon Reduction Action Plan for 2024-2025]. https://www.gov.cn/zhengce/content/202405/content_6954322.htm

UrbanSDK. (2025). The current state of self-driving car regulations in the U.S. https://www.urbansdk.com/resources/the-current-state-of-self-driving-car-regulations-in-the-u-s

Wang, X., Liu, W., & Wang, Y. (2024). 一种新能源报废汽车资源化处理系统及方法 [Yīzhǒng xīn néngyuán bàofèi qìchē zīyuán huà chǔlǐ xìtǒng jí fāngfǎ, A resource treatment system and method for end-of-life new energy vehicles] (Chinese Patent No. CN114273376B). China National Intellectual Property Administration. https://patents.google.com/patent/CN114273376B/zh

Waymo. (2023). On the road to autonomous driving: Safety and simulation. https://waymo.com

Wen, L. (2023, October 31). 新能源汽车回收再生技术装备解决方案 [Xīn néngyuán qìchē huíshōu zàishēng jìshù zhuāngbèi jiějué fāng'àn, New energy vehicle recycling and regeneration technology and equipment solutions]. 青合新碳研究院. https://www.icnce.cn/?p=1219

Xinhua News Agency. (2024). China expands autonomous driving pilot zones in major cities. https://www.xinhuanet.com

Xin Hua She. (2025, January 17). 超3000万辆新能源车奔跑在中国道路上 [Chāo 3000 wàn liàng xīn néngyuán chē bēnpǎo zài zhōngguó dàolù shàng, Over 30 million new energy vehicles are running on China's roads]. 中国政府网. https://www.gov.cn/lianbo/bumen/202501/content_6999345.htm

Xu, K., & Zhou, J. (2019). 一种报废汽车整体资源化处理方法及设备 [Yīzhǒng bàofèi qìchē zhěngtǐ zīyuán huà chǔlǐ fāngfǎ jí shèbèi, A method and equipment for integrated resource treatment of end-of-life vehicles] (Chinese Patent No. CN106807722B). China National Intellectual Property Administration. https://patents.google.com/patent/CN106807722B/zh

Zhang, W. (2024, January 15). The future of artificial intelligence in education. WeChat Public Platform. https://mp.weixin.qq.com/s?__biz=Mzg4MjY2NDgxMg==&mid=2247547755&idx=1&sn=be980b3267d624aaf81d85e183594b62&chksm=ceb8afc3da85347cb094f8245a7e29bf4137ed810e2fd32480c65a6495344e196cb408482132&scene=27